ファイル:Securitization Market Activity.png

{kind=link}

{kind=link}

{kind=link}

元のファイル (960 × 720 ピクセル、ファイルサイズ: 79キロバイト、MIME タイプ: image/png)

ウィキメディア・コモンズのファイルページにある説明を、以下に表示します。

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

概要

|

このファイルのベクター画像 (SVG) が利用できます。 使う目的に対し、元画像よりもSVGがより優れている場合、SVG画像を使用して下さい。

File:Securitization Market Activity.png → File:Securitization Market Activity.svg

|

|

| 解説 |

English: Image from Economist Mark Zandi's FCIC Testimony

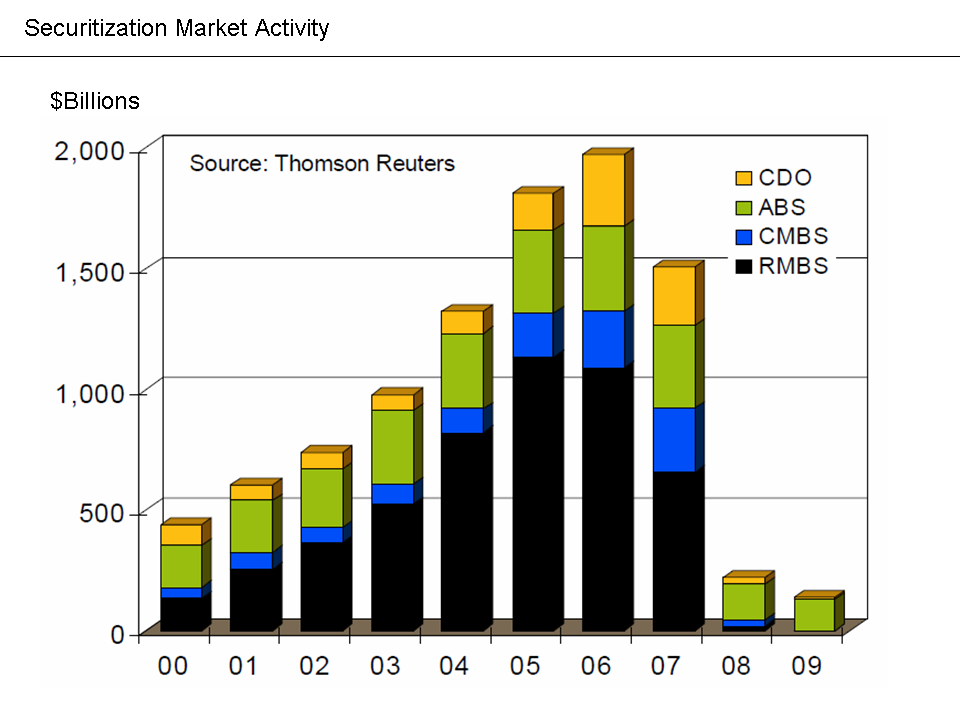

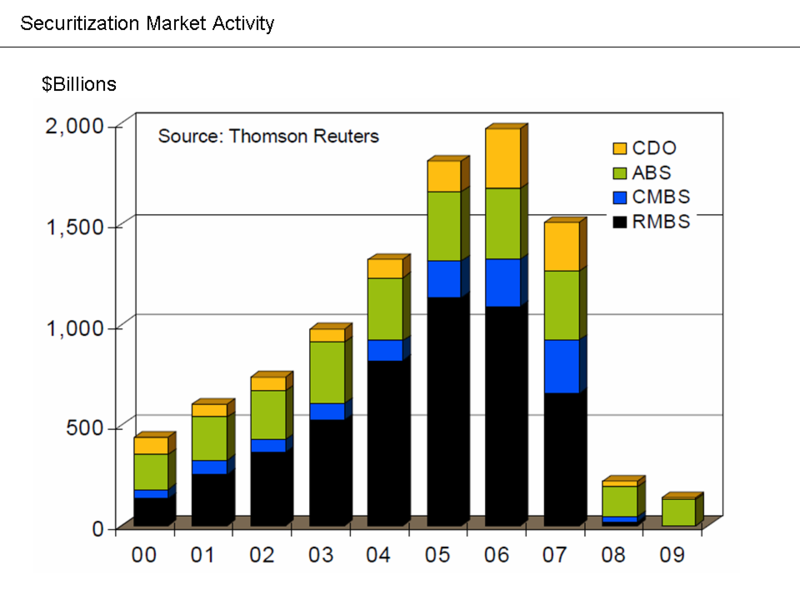

ExplanationFrom Economist Mark Zandi's January 2010 testimony to the Financial Crisis Inquiry Commission: "The securitization markets also remain impaired, as investors anticipate more loan losses. Investors are also uncertain about coming legal and accounting rule changes and regulatory reforms. Private bond issuance of residential and commercial mortgage-backed securities, asset-backed securities, and CDOs peaked in 2006 at close to $2 trillion...In 2009, private issuance was less than $150 billion, and almost all of it was asset-backed issuance supported by the Federal Reserve's TALF program to aid credit card, auto and small-business lenders. Issuance of residential and commercial mortgage-backed securities and CDOs remains dormant."[1] Banks and other financial institutions packaged various types of loans (including mortgages) into securities and sold them to global investors. This is called securitization. In exchange for purchasing the investment, the investor receives a right to the cash flows from the underlying loans specified for the security. The chart shows how this financing source dried-up, meaning that non-prime mortgages and other types of loans could not be originated and sold to investors. |

| 原典 | http://www.fcic.gov/hearings/pdfs/2010-0113-Zandi.pdf |

| 作者 | Farcaster (talk) 04:36, 10 October 2010 (UTC) |

ライセンス

このファイルは、アメリカ合衆国の連邦政府と雇用関係にある公務員がその職務上作成したアメリカ合衆国政府の著作物であり、アメリカ合衆国の著作権法上パブリックドメインに属します (17 U.S.C. §105)。

注意:このライセンスは、アメリカ合衆国政府の著作物についてのみ効力を有します。アメリカ合衆国の各州、郡、その他の地方自治体が作成した著作物に対しては適用できません。

|

| |

| このファイルは著作権法の既知の制約(隣接権や関連する権利を含む)から自由であると特定されています。 | ||

元のアップロードログ

{kind=link}

- 2010-10-10 04:36 Farcaster 960×720× (81241 bytes) {{Information |Description = Image from Economist Mark Zandi's FCIC Testimony |Source = http://www.fcic.gov/hearings/pdfs/2010-0113-Zandi.pdf |Date = ~~~~~ |Author = ~~~~ |Permission = |other_versions = }}

ファイルの履歴

過去の版のファイルを表示するには、その版の日時をクリックしてください。

| 日付と時刻 | サムネイル | 寸法 | 利用者 | コメント | |

|---|---|---|---|---|---|

| 現在の版 | 2010年10月14日 (木) 01:07 | | 960 × 720 (79キロバイト) | Hideokun | {{Information |Description={{en|Image from Economist Mark Zandi's FCIC Testimony<br/> == Explanation == From Economist Mark Zandi's January 2010 testimony to the en:Financial Crisis Inquiry Commission: "The securitization markets also remain impai |

ファイルの使用状況

以下のページがこのファイルを使用しています:

グローバルなファイル使用状況

以下に挙げる他のウィキがこの画像を使っています:

- cs.wikipedia.org での使用状況

- en.wikipedia.org での使用状況

- fa.wikipedia.org での使用状況

- hy.wikipedia.org での使用状況

- it.wikipedia.org での使用状況

- vi.wikipedia.org での使用状況

- zh.wikipedia.org での使用状況

{kind=link}